Roth IRA for Beginners: The Complete 2026 Guide

If you're searching for roth ira for beginners, you're already ahead — most people wait years before taking this step, and that delay costs them tens of thousands in tax-free retirement wealth.

Table of Contents

What Is a Roth IRA for Beginners?

A Roth IRA is an individual retirement account that lets your money grow completely tax-free. You contribute money that has already been taxed, and every dollar you withdraw in retirement — including all the gains — is yours to keep, no taxes owed.

For anyone exploring roth ira for beginners, the core appeal is simple. Pay taxes now at your current (likely lower) rate, and never pay taxes on that money again — even if it grows into hundreds of thousands of dollars.

This makes a Roth IRA especially powerful for younger earners who expect their income — and their tax bracket — to rise over time. You lock in today's lower rate and let decades of compounding do the heavy lifting.

2026 Contribution Limits and Eligibility Rules

In 2026, the Roth IRA contribution limit remains $7,000 per year. If you are age 50 or older, you can contribute up to $8,000 thanks to the catch-up provision.

To contribute, you must have earned income — wages, salary, freelance income, or self-employment income all count. You cannot contribute more than you actually earned that year.

There are also income limits. For 2026, single filers must earn under $146,000 to contribute the full amount. Married filing jointly couples face a phase-out beginning at $230,000. You can verify the latest thresholds directly on IRS.gov.

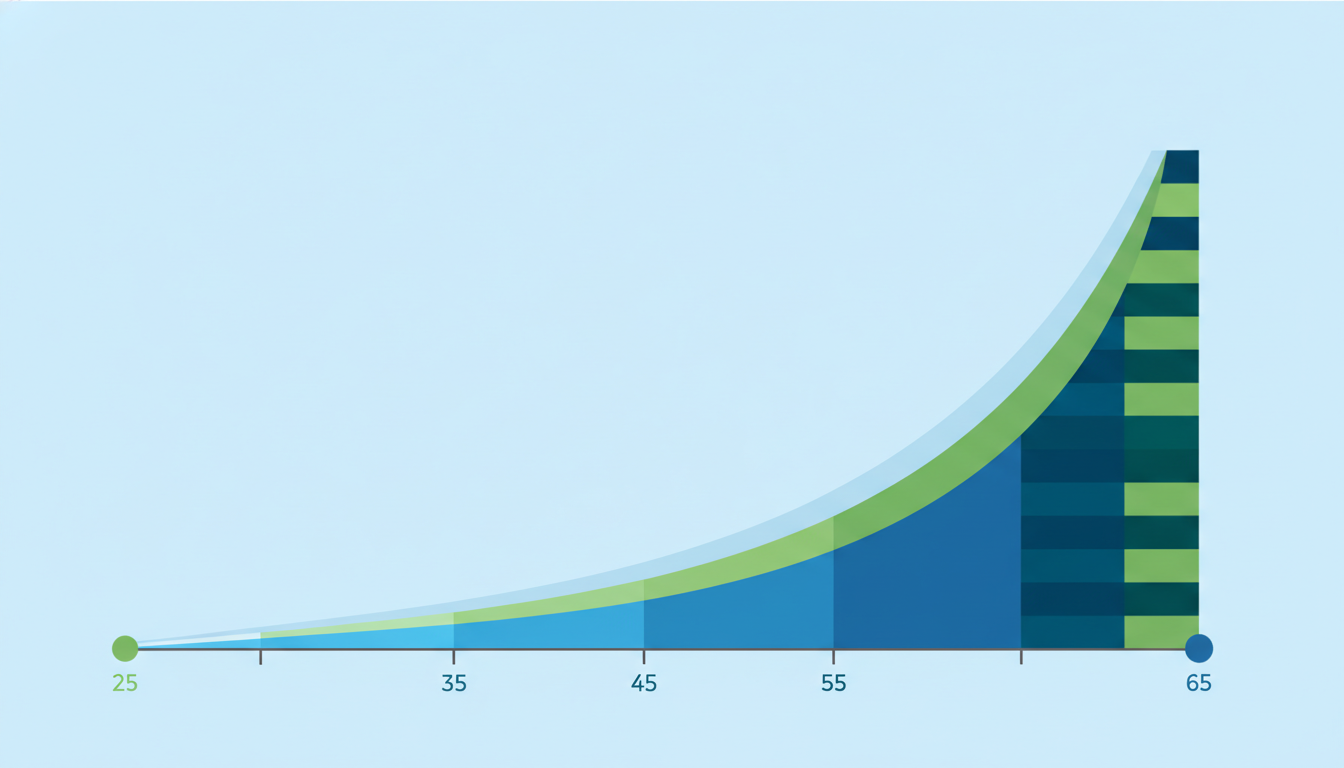

Starting early makes an enormous difference. According to Vanguard, an investor who starts a Roth IRA at age 25 and maxes out contributions annually can accumulate over $1 million tax-free by retirement, assuming a 7% average annual return.

How to Open a Roth IRA for Beginners Step by Step

The process of opening a roth ira for beginners is simpler than most people expect. You do not need a financial advisor or a large sum of money to get started.

Here is exactly what to do:

- Choose a brokerage: Open your account at a reputable, low-cost provider such as Fidelity, Vanguard, or Schwab. All three offer no account minimums and excellent beginner tools. Fidelity's Roth IRA is a popular starting point.

- Complete the application: You will need your Social Security number, a government-issued ID, and your bank account details. The online process takes about 10 to 15 minutes.

- Fund your account: Link your checking or savings account and transfer your first contribution. You can start with as little as $50 — you do not need to contribute the full $7,000 at once.

- Select your investments: This is the most critical step. Do not skip it. Depositing money without choosing investments leaves it sitting in cash earning almost nothing.

- Set up automatic contributions: Schedule a monthly transfer — even $200 a month adds up to $2,400 a year. Automation removes the decision fatigue and keeps you consistent.

Why the Investment Selection Step Matters Most for Roth IRA Beginners

One of the most common and costly mistakes in roth ira for beginners is confusing opening the account with actually investing. Many new account holders deposit money and assume it is automatically invested — it is not.

When you log in after funding your account, you must actively choose what your money buys. If you skip this step, your funds sit in a low-yield cash position and grow almost nothing, defeating the entire purpose.

Best Investments to Put Inside Your Roth IRA

For anyone navigating roth ira for beginners, the investment decision does not need to be complicated. Experts consistently recommend starting with low-cost index funds or ETFs.

An S&P 500 index fund gives you instant exposure to 500 of the largest U.S. companies in a single investment. It is diversified, low-cost, and has historically delivered strong long-term returns. According to NerdWallet, these funds are among the top choices for new Roth IRA investors.

Here are smart investment options to consider inside your Roth IRA:

- S&P 500 Index Fund: Tracks the top 500 U.S. companies. Low fees, broad diversification, and a proven long-term track record.

- Total Market Index Fund: Covers the entire U.S. stock market, including small and mid-cap companies, for even wider exposure.

- Target-Date Fund: Automatically adjusts your asset mix as you approach retirement. Ideal if you want a fully hands-off approach.

- International Index Fund: Adds global diversification by including stocks from developed and emerging markets outside the U.S.

The most important factor is keeping fees low. Even a 1% annual fee difference can cost you over $100,000 in lost growth over 30 years. Always check the expense ratio before investing.

Common Mistakes Beginners Make With a Roth IRA

Understanding roth ira for beginners means knowing what to avoid just as much as knowing what to do. These mistakes are easy to make and hard to recover from.

Waiting too long to start. Every year you delay is a year of tax-free compounding you can never get back. A 25-year-old who starts investing has a massive advantage over someone who starts at 35 — the math is that straightforward.

Contributing more than you earn. If your earned income is $4,000 for the year, you cannot contribute $7,000. The IRS caps your contribution at your actual earned income for the year.

Withdrawing early. Roth IRA contributions (not earnings) can be withdrawn any time without penalty. But pulling out investment earnings before age 59½ typically triggers taxes and a 10% penalty. Leave it alone and let it grow.

Not contributing consistently. Missing contributions for several years can significantly reduce your final balance. Even small, regular contributions beat large, irregular ones. For deeper reading on managing your retirement accounts, explore our financial guides for more strategies.

Ignoring the account after opening it. A roth ira for beginners is not a set-it-and-forget-it product at the start. You need to fund it, invest it, and review it at least once a year to make sure your allocations still match your goals.

Why Starting a Roth IRA in 2026 Is One of the Best Moves You Can Make

The power of a Roth IRA comes down to time and tax-free compounding. Every dollar you invest today grows without the drag of future taxes eating into your gains.

For anyone exploring roth ira for beginners in 2026, the window to act is right now. Contribution limits are fixed — if you miss this year, you cannot go back and top it up later. Each year is a use-it-or-lose-it opportunity.

The difference between someone who maxes out a Roth IRA every year starting at 25 versus starting at 35 can easily exceed $400,000 by retirement. That is not a small detail — that is a life-changing amount of money.

Check out our more articles on retirement planning and investing to keep building your financial foundation. If you want actionable strategies beyond the basics, read more tips from our retirement category.

Final Thoughts on Roth IRA for Beginners

Opening and maximizing a Roth IRA is genuinely one of the highest-leverage financial decisions you can make as a young adult. The rules are straightforward, the account is easy to open, and the long-term payoff is exceptional.

Start with a trusted brokerage, fund your account, invest in low-cost index funds, and contribute consistently. That is the entire formula for roth ira for beginners — and it works.

For more detailed guidance on account rules and tax treatment, the Investopedia Roth IRA guide is an excellent reference to bookmark alongside this article.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always consult a qualified financial advisor before making investment decisions.